Monetary Policy

TLDR: When money supply × velocity changes unexpectedly, it can cause immense economic damage. Utopians are Market Monetarists, who use prediction markets to stabilize inflation.

Prerequisite: Price Controls

Money is, in essence, a way of tracking and comparing debt. In a pre-money society, the most common form of trading is to have one party do a thing and the other party “owe them one.” This owing-a-favor is also a kind of debt, though it’s terribly hard to quantify. Two favors don’t necessarily cancel-out, since favors can be attached to a variety of different costs and benefits. Tracking favors requires mental effort, it’s hard to trade favors between people, and this system of debt is hard to scale beyond small bands of people where everyone knows everyone.

These problems can be alleviated with money: the evolved form of favor-trading. Some people tend to conceptualize money more through the frame of trading concrete objects, like food and tools, in large part perhaps because primitive money has tended to arise from the exchange of value-dense commodities like salt and gold. But bartering for specific goods (or services or whatever; for brevity I’m just going to say “goods” in this essay) is very different from trading using money. If I trade you a book for an apple, it’s because I want the apple more than the book and you want the book more than the apple. No trust is needed beyond the basics of that one trade; there’s no sense in which either of us have to be “paid back.” But if I buy an apple with coins, you probably don’t want the coins in themselves. Instead, you trust that you can later trade those coins for something better than an apple (from your perspective).

Money, like all debt, relies on trust to function, though that trust can rest on a society or institution, rather than an individual. Whenever a sale happens, it’s thanks to the seller trusting in future compensation for their lost good. Workers sell their time/energy/skill at some job, then benefit from that sale later, sometimes years later, when they make a purchase of some other good, like housing or entertainment. Just like a favor, money only works if someone makes two exchanges: a sale followed by a purchase.

Money on Fire

Because money is a measure of debt, destroying money is a kind of debt-erasure. If a rich person burns a billion dollars in a bonfire (or forever loses the key to a billion-dollar bitcoin wallet), they’ve essentially released the debt that society owes them, saying “no need to compensate me for what I gave you earlier.” In many ways, this is identical to a donation of the same amount of money. Money-destruction is charity.

Who benefits from this charity? Well, let’s consider the consequences of the act. Let’s say that instead of burning the money, the billionaire would have used it to bid on a variety of pieces of artwork at auction. In the world where those bids are placed the art sells for more, and in the world where the bills were burned it sells for less (regardless of whether the billionaire wins the auctions). So directly, the competitors at auction benefit from the bill-burning, both in being more likely to get the scarce good (less shortage), and/or in not having to pay as much for it (lower prices). But there’s an indirect effect as well: the sellers of the artwork get less money in the bill-burning world, and so they go on to have fewer dollars to use to compete for other goods down the road. Then whomever they’d have given their dollars to has fewer dollars, and so on.

This dynamic, where the absence of dollars (compared to the counterfactual) causes a reduction in prices in a variety of markets as it spreads through the economy, is called deflation. (Or rather, “deflation” refers to falling prices, regardless of the reason. In this essay we’ll be focused on deflation entirely connected to how much money there is, and mostly ignore other factors that affect price.) The true recipients of the bill-burning-billionaire’s charity are the people who hold dollars when the prices go down (compared to the counterfactual).

Note that the relevant quantity is the number of dollars that are being used for competition in the marketplace. A dollar in an auction is used if it drives up the price (regardless of who wins the auction), and in general we can measure the number of dollars in play by tracking the total number of dollars that change hands.

This means it turns out to be totally irrelevant whether the billionaire burns the money or hoards it in a mattress for a hundred years: those dollars are out-of-circulation. The fewer dollars that circulate in a given period, the lower the prices tend to go.

Total Nominal Income

Since we care about how many dollars are being actively used, we can see another important fact: if a seller saves the money they get in a trade, that money only gets to be counted for that sale. If instead the seller had gone on to spend that money again, and perhaps their trading partner uses it again, and so on, that money continues to apply competitive pressure that keeps prices high. We can thus approximate the quantity of active dollars by multiplying the total number of dollars that exist by the average number of transactions-per-dollar in the relevant period. Or, perhaps more easily, we can simply sum up the dollar-amounts for each sale that occurs.

This sum — the driver behind widespread changes in prices — is sometimes mistaken for Nominal Gross Domestic Product (NGDP). What we actually care about is total expenditures/income across all people who use a currency, but NGDP only applies within the borders of a specific country, and only to “final products” like bicycles, not “parts” like bicycle wheels. Still, NGDP is very close to what we’re interested in, and it’s worth paying attention to because it’s so popular and well-measured. Because I want to be precise, let’s name the thing we’re really interested in the Total Currency Throughput (TCT)1 and remember that NGDP is a (reasonably good) approximation.

Thus, when our billionaire burns those bills, we don’t immediately care. What we (and the billionaire!) care about is that our billionaire isn’t spending money that would otherwise have been spent. This change in spending (unexpectedly) drives down the TCT, which creates a wave of surpluses throughout the economy (fewer dollars being spent at fixed prices = fewer goods being sold), which eventually convinces sellers to lower their prices. Deflation in action!

The Problems of Deflation

The theory of deflation doesn’t sound so bad. Sure, there’s less money bouncing around, but eventually people figure it out and cut prices to match. If everyone woke up one morning and every money quantity, from wages to bank accounts to gas prices, was halved, there’d be no real issue. The units of money are mere symbols, after all — the value of those amounts of money as expressed in real goods would remain unchanged.

The reality of deflation is far worse. First, it takes time for an economy to adjust to a decreased level of active money, and that period can be quite painful. After TCT has dropped but before prices go down, people just randomly can’t afford as much at any given time and usually don’t know why.

Businesses in the short term will make less money than expected, not realizing that they need to cut prices, and sometimes they’re unable to cut prices until their suppliers do the same (and/or their workers’ pay is cut). At the same time as deflation may be happening, other changes may be happening in the world as well. This leads some investors to make poor decisions via hallucinating that the price dip is the result real-world changes like technological improvements, changing fashions, or loss of faith in particular products. Complex economies are thus particularly hard-hit by this shock to the money supply, as it can take years for the relevant info to propagate through the system and for people to cease being confused by the change.

Meanwhile, those with negative sums of money in the form of debt are screwed by deflation. Not only do debtors have less money to make payments in the short-term, but debt contracts usually don’t have an inflation adjustment clause, meaning that their debt (as measured in real goods, like apples) grows as deflation occurs. Creditors (and especially pensioners) are theoretically on the benefitting end of this shift, but in practice steep deflation tends to result in defaulting on loans, which obviously hurts creditors as a group.

It gets worse. Because money depends on trust to function, whenever there’s economic chaos (like from a severe cut to TCT) people tend to save more and spend less… further lowering the TCT. This is then exacerbated when people realize prices are going down across the board, because they correctly reason that they’ll have more purchasing power with their money down the line compared to if they spend it immediately. These dynamics form positive-feedback-loops that can break entire economies, ruining trust and preventing trade.

But it gets even worse still! Prices in general are “sticky” in the sense that it takes a while after the money supply shrinks for people to figure out what’s happening (specifically: to figure out that it’s not temporary noise) and actually go through the trouble of changing all the labels on their goods. But wages are extremely sticky. Why? Because people often feel that pay cuts are personal, and are an attack on their abilities as a worker. Here’s a good 4-minute video by Marginal Revolution University:

As a result of sticky wages, employers who experience a bad year are much more likely to lay off employees than to cut wages across the board (especially in the presence of price floors, such as union deals or minimum wage). While a change in wages may be somewhat disruptive, in theory it’s compensated by the falling prices elsewhere in the economy. Unemployment, however, is a huge cost and loss of real-world productivity and value, which can fuel a recession in yet another positive-feedback-loop.

Money Go Up

What about an increase in TCT? The previous logic still applies, just in reverse. More money in competition for the same goods will eventually drive an increase in prices, a.k.a. inflation. If decreasing TCT/deflation tends to be bad, perhaps the opposite is good? Unfortunately, it’s not so simple.

Remember, much of why deflation is bad is because it takes a while for an economy to adjust to the new quantity of money in people’s pockets. This phenomenon is still at play with inflation, where instead of surpluses due to prices being too high, inflation can cause an initial round of shortages from the prices being too low. Price ceilings can make this a long-term problem, causing persistent shortages and/or reductions in quality. Price confusion also still applies, where instead of hallucinating reasons for prices to go down, investors form false (or at least incomplete) hypotheses for why prices are going up. Higher prices than expected can cause reductions in trading, as buyers suspect that the abnormally-high prices will soon go back to normal.

Furthermore, just as deflation is a small gift of purchasing power to people who are holding cash when prices drop, inflation is the opposite: a purchasing power tax on cash-holders. Wealthy people tend to have most of their wealth stored in assets like land and businesses, but the same is not true of the medium-poor, who tend to hold more cash as a fraction of total wealth.

People (or governments!) who are in debt (i.e. have negative money) benefit from unexpected inflation, but creditors, pensioners, and retirees will find themselves with less purchasing power than expected. These effects can be mitigated by savvy deal-makers, however, either by including inflation adjustment clauses in their contracts or by predicting inflation and pricing it into the interest rate/payment schedule.

Most economists, however, believe inflation to be much less of a problem than deflation, and often think it’s no problem at all when it’s predictable. Where predictable deflation causes people to avoid spending in order to have their dollars go further in the future, predictable inflation means dollars a naturally worth less and less with each passing second. This can encourage spending, nudging people towards making more purchases. As long as a trade is win-win, real wealth is created, so it’s far better to encourage trading with an inflationary currency than encourage hoarding with a deflationary one. Saving for the future in an inflationary regime is still possible by buying stocks or bonds (with sufficient interest rates), just not holding cash per se. Credit and investment is thus plentiful in inflationary regimes, which can spur new ventures, albeit with some bias towards risk if the inflation is too intense.

Finally, when the TCT is steadily increasing, wages tend to be less sticky. Employers can raise the wages of the best employees, giving a boost to their morale, despite the wage-increase being purely symbolic (not a reflection of real purchasing power changing). Meanwhile, an employer can keep the nominal wage for bad employees the same, effectively cutting their real wage, but possibly without even hurting their feelings.

Throughput Disasters

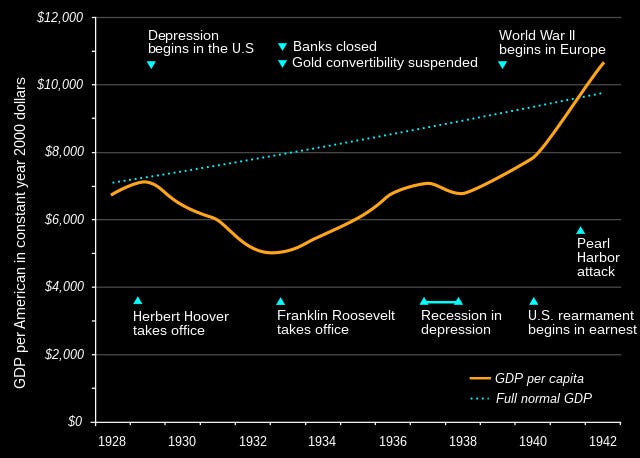

Unexpected changes in TCT are behind some of the worst crises in recent times. The Great Depression had many contributing factors (e.g. the dust bowl), but one of the biggest was that as the stock market crashed, people started to want to hold more cash and avoid spending. The TCT thus tanked, causing businesses everywhere to not have enough money to pay their employees, which caused mass-unemployment. Debtors — mostly new businesses or mortgage-holders — didn’t have the money to pay their debts, and had their lives and livelihoods dismantled by desperate creditors. Skilled laborers searched hopelessly for jobs while factories sat idle. Fear kept spending low in the beginning, and general poverty kept spending low even as prices dropped. Even those lucky enough to have cash held most of it back, not wanting to lose everything like their neighbors had.

(Some claim that a big part of the drop in the money supply was caused by fractional reserve banks failing due to bank runs. This seems overstated to me compared to personal spending choices. Banks that failed surely drove a lot of chaos and fear, and I don’t want to understate that on causing consumers to hoard or randomly go broke. But dollars held in savings accounts weren’t actually directly contributing to the TCT, just making people feel more safe to spend their paychecks. It doesn’t matter how much broad money an economy claims to have; it matters how many dollars are actually being put to work.)

Eventually a combination of downwards-adjusted prices (especially wages), government spending (increasing TCT), and reduced economic fear (perhaps related to the start of WW2) got people to trade and work with each other again.

The key here is not so much that “we spent our way out of the depression,” which makes it sound like the problem was a great social debt had to be repaid to God by wasting people’s time digging ditches. Someone spending money means someone else earning money, and it’d be just as true to say “we earned our way out of the depression.” But both of these are half-frames. The real story is that TCT (and GDP) is a measure of how much people are trading with each other, and it was people making win-win trades that brought the economy back. Big government spending/borrowing wasn’t useful because those specific government projects were necessary, but because it meant there was suddenly enough money flowing through the system again for people to feel comfortable investing, hiring, and spending.

This same story — not enough money — was behind The Great Recession of 2008. The 2008 recession was kicked off by a failure of large financial institutions to manage risk well, but putting the blame for the recession on Lehman Brothers and Goldman Sachs is a mistake. In a world where things had been managed more appropriately, the damage of those poor investments would have been limited to (the inept parts of) the financial industry and some poor souls who borrowed beyond their means. Instead, the American people and much of the rest of the world suffered en masse.

I claim that recessions/depressions in general are the product of bad monetary policy. If there were a way to ensure that year-after-year a predictable number of dollars were spent, then the failure of specific businesses, financial institutions, et cetera would not have the effect that we tend to see on widespread unemployment, debt defaulting, and poverty. And thankfully, there is an easy way to make sure TCT is smooth and predictable.

Utopian Monetary Policy

My guess is that Utopians are less irrational than the people of Earth in 2023. In particular, they study more economics and tend to pin the prices of their salaries/wages/loans/etc to an average basket of goods, so that they’re more stable in the face of inflation/deflation. This makes prices, especially wages, less sticky in Utopia.

But it’s still nice to see numbers smoothly go up. Utopians are human, after all. And recalculating prices based on local-information is harder than simply increasing the prices of goods a little bit each year. So to support the number-go-up bias and provide more stability, currencies in Utopia are controlled by a central bank2 to have a predictable TCT.

Each currency has a target TCT that’s a function of time, usually on the order of 5% annual growth from some fixed starting value. The target TCT is totally blind to all actual TCT values; it’s just a static equation. So if the observed TCT is below-target one-year, the target next year will be more than 5% higher than the observed level. Every medium-short period of time, a futarchy-esque prediction market is created where people can make bets with each other about what the central bank will have done, conditional on the target TCT being pretty close to the observed TCT. Specifically, contracts on that market transfer an amount of money from one party to another (ideally in a different currency) that scales based on how much money the central bank creates/destroys during a specific period, where the contracts are nullified/refunded if the TCT doesn’t get near the target. Then, the central bank simply creates or destroys an amount of money that corresponds to the market’s price.3

For example, let’s say that the central bank wants to hit 5% annual growth with a 4T (four-trillion units of currency) TCT baseline in 1984. Now it’s 2023, so the target TCT for this year is 4T×exp(5%×(2023-1984)) ≈ 28T. But let’s say that the currently-observed TCT is 27T. The prediction market is for contracts that read “If the observed TCT for 2023 is 28T, this contract’s seller will transfer X dollars to the buyer, where X is the net number of billions of currency-units created by the central bank in 20234. In the case that the target was hit, but the central bank destroyed currency (on net), the transfer goes from buyer to seller instead5. If the target is not hit, sale of this contract is reversed with full refund.” And in our example, let's say that there's a bid/ask spread on the market with the halfway-point being priced at $52, indicating that the market believes the central bank ought to create more money-units.

Let’s say Alice sells a contract to Bob at $52, the central bank ends up eventually creating 83B in 2023, and hits its target. Then Alice would need to give Bob $83, meaning Bob got $31 on net. Let’s say that later in that year Carrol sold Dave a contract for $99. Since the central bank still ended up hitting its target with +83B, she gives him $83 back, netting him -$16. Thus when the market price is higher than the true value, savvy traders will sell, driving the price down. But if the market price is lower than the true value, savvy traders will buy, driving the price up. This means that when the price stabilizes, it reflects the aggregate wisdom of the world’s experts. The central bank, in our example, ended up creating 83B because at a certain (semi-random) point in time, the average market price stabilized to around $83.

How is money created or destroyed? The US Federal Reserve does this through buying and holding stable assets like treasury bonds. When a bond is purchased (at market prices) new dollars enter the economy, increasing the TCT. Conversely, selling a previously-purchased bond back to the public puts currency into the reserve, taking it out of circulation, and decreasing the TCT.

In Utopia I worry that the predictable, large-scale buying of assets like bonds would cause them to be slightly overpriced and/or bias entities like governments towards borrowing money. Instead, I think it’s probably best to create currency by having the central bank occasionally contribute to basic income which is then evenly distributed to all people. This probably offsets the unfairness of inflation being a hidden tax on people who hold cash (the lower-middle class), and feels generally egalitarian. Currency destruction could be done through a flat sales tax/VAT/income tax that takes a small amount every time currency changes hands (regardless of why it’s changing hands). I’m less confident about the specifics of how best to increase/decrease the amount of flowing currency than I am that the central bank should somehow do this to stabilize the economy.

As a result of the automated management of the money supply, Utopia has a very consistent amount of money flowing through the economy from year to year. This means, despite inflation adjustment clauses being more common, they’re less necessary, as general inflation follows a very predictable path on the scale of decades. Occasionally there is a natural disaster or a scandal that disrupts various parts of the economy, but the Utopian central bank creates huge quantities of money during these events to encourage people to keep trading rather than withdrawing in fear, then taxes it away once the dust settles and people are less spooked. Utopia has no recessions or depressions or inflation crises.

Utopian banks do not do any fractional-reserve nonsense. Instead banks simply sell bonds that they’re contractually obligated to buy-back at any time for an amount that scales exponentially with the age of the bond. This is equivalent to fractional reserve in practice, but is more explicit about what’s happening. Banks are also legally required to have buyback insurance, in case there’s a bank run. A portion of the buyback insurance payout might be be subsidized by governments in order to protect account holders in the case of a widespread disaster, but the presence of some insurance premiums serves as an incentive gradient to discourage risky/bad investments.

The Utopian economy grows at a steady clip, with financial failures resulting in certain people in the financial industry getting fired and little else. Unemployment is lower in Utopia — a result of less wage stickiness and absence of recessions. The average person usually takes the well-being of the economy for granted and is happier as a result.

TCT is also related to, but not the same thing as aggregate demand. Aggregate demand is a function that takes a price level and returns a dollar figure. TCT is the minimum of the aggregate demand and aggregate supply functions at the current price level. If someone knows what TCT is actually called in the literature, please leave a comment.

TCT control can be implemented for both centralized fiat-currencies and decentralized cryptocurrencies. The “central bank” for a cryptocurrency is the blockchain software itself; simple control mechanisms can be directly built into the code. Actual TCT can be very easily measured on crypto by just summing up all the transactions within a given timeframe.

Market manipulation is a risk, since the refunding of contracts means that a wealthy manipulator (e.g. a hostile government) could push the central bank off-target and then not have to pay. An easy solution to this is have a second prediction market for whether the TCT target will be hit, then cap trader’s risk in the central bank market at some multiple of that trader’s “yes” position on the will-the-target-be-hit market.

To limit risk, the value of X might be clamped to a certain range. If the price of contracts ever gets close to one of the extrema a new market can be created where X is offset to be the amount of currency created/destroyed minus/plus some constant.

Negative transfers from “seller” to “buyer” are going to typically be associated with negative contract prices on the market. Thus the “buyer” receives money from the “seller” in exchange for signing the contract. So in our example a -$10 market price for contracts corresponds to an expectation that the central bank will destroy 10B.

This essay implicitly supports level targeting, but my guess is that it doesn't emphasize it enough. Here's Sumner's perspective: https://www.themoneyillusion.com/why-level-targeting/

A friend of mine just pointed out that the case for a monetary policy of positive-growth NGDP targeting is largely that it allows employers and debtors to continue to be able to pay, even when productivity drops from some supply shock (e.g. a pandemic). But consider the case where the population grows sharply, due to a change in immigration policy. This will create excess demand for dollars, leading to a de-facto deflationary situation that could destabilize contracts even while NGDP is increasing! As a result, my guess is that NGDP/capita, or even better, NGDP per hour of (human?) labor is a better monetary target.